Real Personal Income, Metropolitan Price Parities & Inflation

Posted on 06/04/2019 by Beverly Kerr

- In 2017, Austin saw strong growth of 4.1% in real (price-adjusted) total personal income, an important, broad-based measure of the economy—Austin's growth was fifth best among the 50 largest U.S. metros.

- Austin’s 1.4% real per capita personal income growth in 2017 lagged most major metros, ranking 35th, but that rate exceeds performance on the measure in Dallas-Ft. Worth, Houston and San Antonio.

- Overall price levels in Austin are just 0.5% higher than the U.S. average.

- U.S. inflation was 1.8% in 2017. The rate was 1.9% for Texas and 2.1% for Austin.

Real, price-adjusted estimates of personal income[1] for states and metropolitan areas for 2008-2017 were released by the U.S. Bureau of Economic Analysis in mid-May. Austin saw relatively strong real personal income growth in 2017 (4.1%), while Texas’ growth (2.1%) fell below the pace of growth nationally (2.6%). Austin’s 4.1% growth places it fifth among the 50 largest U.S. metros. San Antonio, Houston and Dallas-Ft. Worth grew 2.6% (28th), 2.3% (33rd), and 2.1% (39th) respectively. Among major metros, the greatest gain was 4.8% in Oklahoma City, followed by Jacksonville, New York, and Seattle. No large metros had negative real personal income growth in 2017.

On a per capita basis, 2017 real personal income growth was 1.8% nationally. Texas’ real per capita personal income increased 0.8%. All of the 50 largest U.S. metros saw positive growth in 2017, ranging from 0.1% in Dallas-Ft. Worth to 4.0% in New York. Among Texas major metros, Austin did best in 2017—1.4% (35th). The gain in Houston was 0.9% (43rd) and in San Antonio was 0.7% (48th).

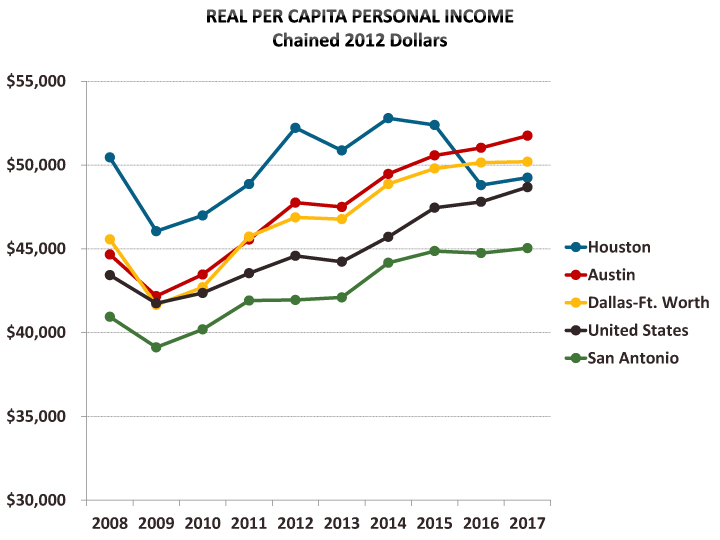

While Austin and the rest of the state appear to have had a lackluster 2017 on the basis of improvements in per capita income, Austin’s gains over the longer run are relatively robust. Austin’s 15.9% real per capita personal income growth since 2008, before the impact of the Great Recession, ranks 11th. Over that period, national real per capita income is up 12.1%.

The greatest gains since 2008 were in San Jose (32.9%), San Francisco (23.6%), and Nashville (23.0%). Dallas-Ft. Worth and San Antonio have gained 10.2% and 10.0% respectively (ranking 32nd and 33rd). In real terms, per capita income in Houston is 2.4% below what it was in 2008. Charlotte is the only other large metro with 2017 per capita income below (by 3.5%) 2008.

This release of real personal income estimates is only the sixth official release of such statistics for metropolitan areas. Something that makes the data particularly innovative and valuable is that the data is not simply inflation-adjusted. The price-adjustments are based on both regional price parities (RPPs) and on BEA’s national Personal Consumption Expenditure (PCE) price index.

RPPs measure geographic differences in the price levels of consumption goods and services relative to the national average,[2] while the PCE price index measures national price changes over time. Using the RPPs in combination with the PCE price index allows for comparisons of the purchasing power of personal income across regions and over time.

According to the BEA, "Americans looking to move or take a job anywhere in the country can compare inflation-adjusted incomes across states and metropolitan areas to better understand how their personal income may be affected by a job change or move. Businesses considering relocating or establishing new plants also now have a comprehensive and consistent measure of differences in the cost of living and the purchasing power of consumers nationwide.”

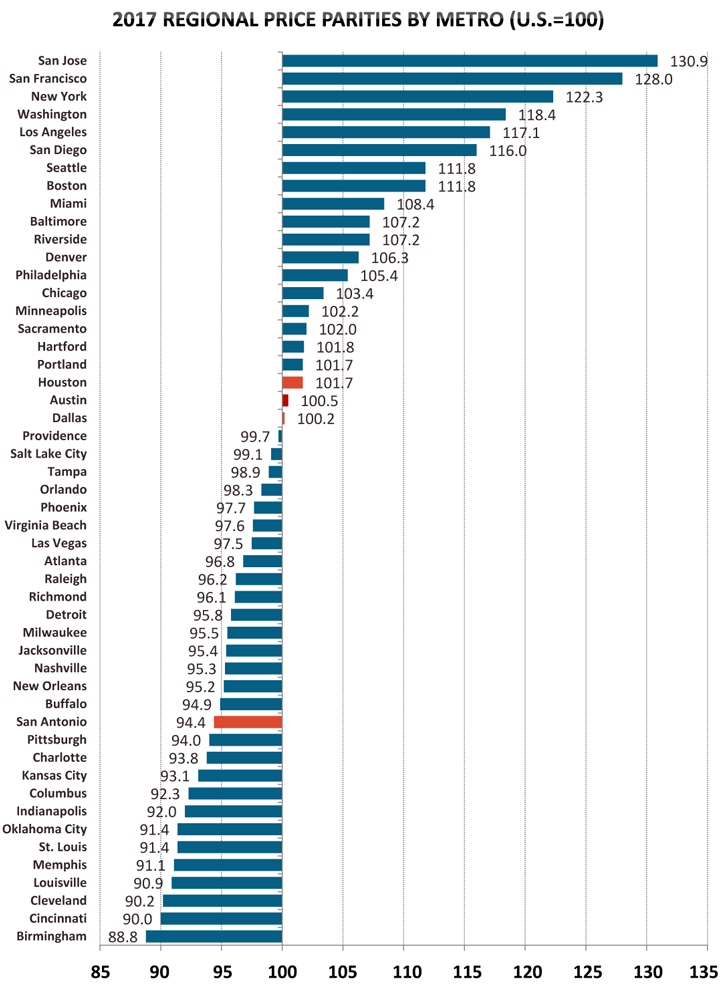

Austin’s RPP in 2017 is 100.5, meaning that on average prices are 0.5% higher than the U.S. average. Austin’s nominal or current dollar per capita income is $54,817 in 2017 and Baltimore’s is $59,797. If you divide Austin’s income by 1.005 and you divide Baltimore’s by 1.072 (each metro’s RPP divided by 100), the RPP-adjusted per capita incomes are $54,544 and $55,781 respectively. That is, the purchasing power of the two incomes is relatively comparable when adjusted by the areas’ differing price levels.

To create real, price-adjusted incomes for a region, current dollar income is divided by the region’s RPP and by the national PCE chain-type price index. The implicit regional price deflator (IRPD) will equal current dollar personal income divided by real personal income in chained dollars.

Thus, the BEA combines RPPs with the national PCE price index to create unique regional price indexes—IRPDs—for each metropolitan area. The growth rate or year-to-year change in the IRPDs is a measure of regional inflation.[3]

U.S. inflation was 1.8% in 2017. Among large metros, inflation ranged from 1.2% in Virginia Beach to 2.9% in San Jose. Austin’s rate was 2.1%, and the statewide rate was 1.9%. Austin’s 2.1% increase in prices ranked eighth highest among the 50 largest metros. Dallas-Ft. Worth’s gain was also 2.1%, while increases in Houston and San Antonio were 2.0% and 1.7% respectively.

Over 2012-2017, prices increased a total of 8.2% in Austin, compared to the national increase of 5.6%. Austin’s increase ranked sixth highest among large metros. Houston, San Antonio and Dallas-Ft. Worth had less inflation than Austin, 7.4%, 6.5% and 6.0% respectively. For inflation over the last five years, San Jose tops the ranking with 13.4% and Chicago ranks 50th with a 3.0% increase.

Austin’s nominal or current dollar per capita personal income is $54,817 in 2017, which is 106% of the national per capita income ($51,640). In the real, price-adjusted series, Austin’s per capita personal income in chained 2012 dollars is $51,754, which is also 106% of the national figure ($48,684). Among major metros, San Jose has the nation’s highest per capita income, both nominal and real. The current dollar per capita personal income for San Jose in 2017 is $96,623, which is 187% of the U.S. current dollar per capita income. However, in real, price-adjusted chained 2012 dollars, San Jose’s per capita income is $70,053 and only 144% of real U.S. per capita income.

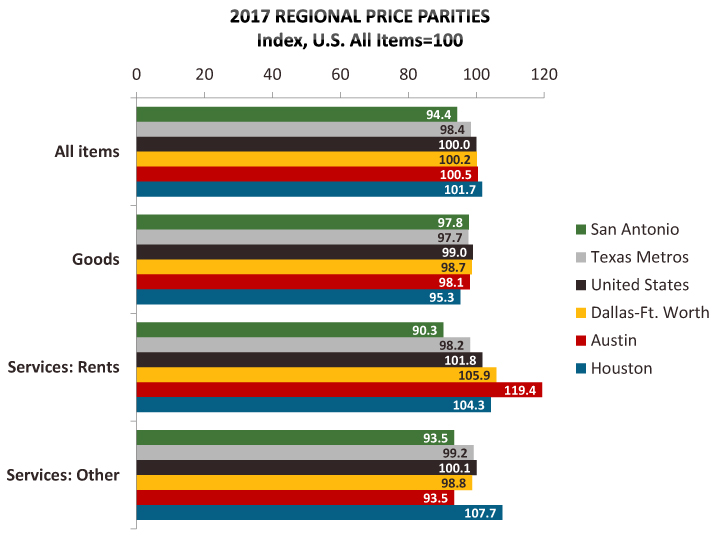

The RPP data made available by the BEA includes separate RPPs for consumption goods and for services, with services broken out into rents and other. Weighting is said to vary by year and is not included with the data, however the BEA notes that states with high (low) RPPs typically have high (low) price levels for rents. A BEA working paper indicates goods account for about one third and services for about two thirds of household expenditures, and that rents account for 29.5%.

Among large metropolitan areas, the All Items RPP ranges from 88.8 (Birmingham) to 130.9 (San Jose). Austin’s RPP of 100.5 is on the high end of the middle range of the distribution of the 50 largest U.S. metros (19 are higher and 30 are lower).

- Goods RPPs have a relatively narrow range of 94.9 (St. Louis) to 112.2 (San Francisco). Austin’s RPP for goods is 98.1, below the nation (99.0) and just above the metropolitan portion of Texas (97.7).

- Rents RPPs range from 68.3 (Birmingham) to 218.4 (San Jose). Austin’s RPP for rents is 119.4, above both the nation (101.8) and Texas metros (98.2).

- Other Services RPPs range from 91.3 (Cincinnati) to 117.7 (New York). Austin’s RPP for other services is 93.5, below both the nation (100.1) and Texas metros (99.2).

FOOTNOTES:

- Personal income is the income received by all persons from all sources. Personal income is the sum of net earnings by place of residence, property income, and personal current transfer receipts. ↩

- RPPs are calculated using price quotes for a wide array of items provided by the Bureau of Labor Statistics Consumer Price Index program, combined with data on rents from the Census Bureau's American Community Survey, with expenditure weighting constructed from the BLS Consumer Expenditure Survey and the BEA's Personal Consumption Expenditures. ↩

- The U.S. Bureau of Labor Statistics produces metro area price deflators for a small number of large metros including Dallas and Houston, however, Austin has never been one of these. ↩

Related Categories: Central Texas Economy in Perspective