RSM monthly GDP index: Negative real growth continues into the second quarter

Posted on 06/25/2020 by RSM US LLP

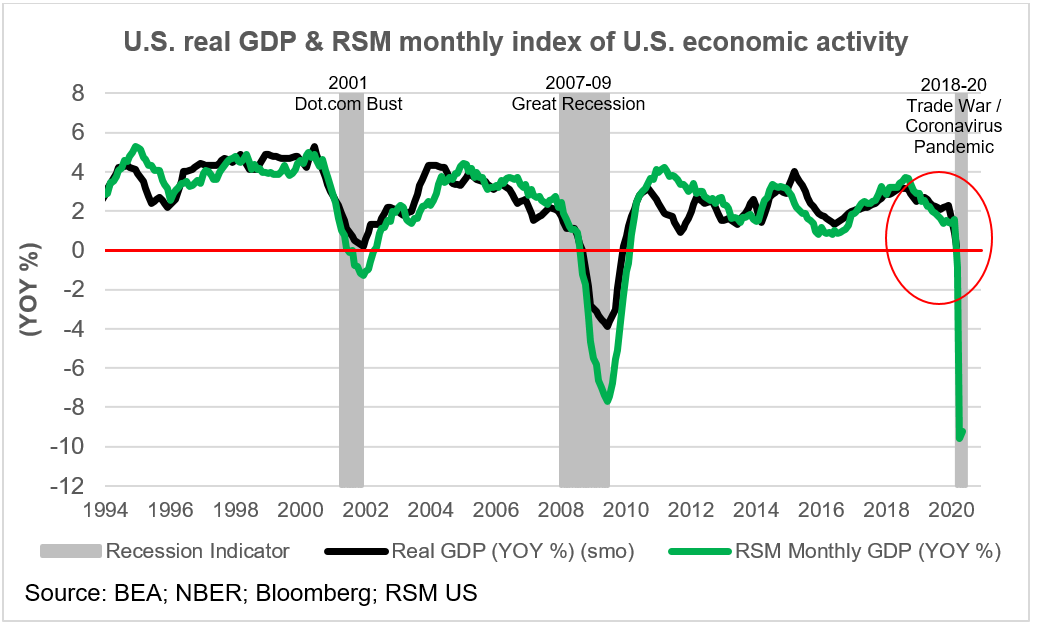

The RSM monthly index of real GDP growth that turned negative in March has now dropped below levels recorded during the financial crisis and Great Recession of 2007-9.

We anticipate that the decline in second-quarter U.S. gross domestic product will be the largest single decline in the modern economic era. Based solely on domestic consumption and manufacturing activity, our monthly index indicates that the U.S. economy hit bottom in April and stayed there in May.

With all indicators reported for April, the RSM index points to real GDP dropping by 9% relative to last year at the same time. Releases of industrial production and labor market data for May — combined with forecasted values for other indicators — suggest that 9% loss carrying over into May as shown in the figure below.

This is the foundation of our estimate of a decline of 38.5% in U.S. second-quarter GDP on a seasonally adjusted annualized pace.

By comparison, the Atlanta Fed’s GDPNow forecast for the second quarter is a 45% decline. The New York Fed’s Nowcast is calling for a 19% decline in the second quarter and a 1.9% decline in the third quarter. These forecasts are based on the release of economic data throughout the quarter.

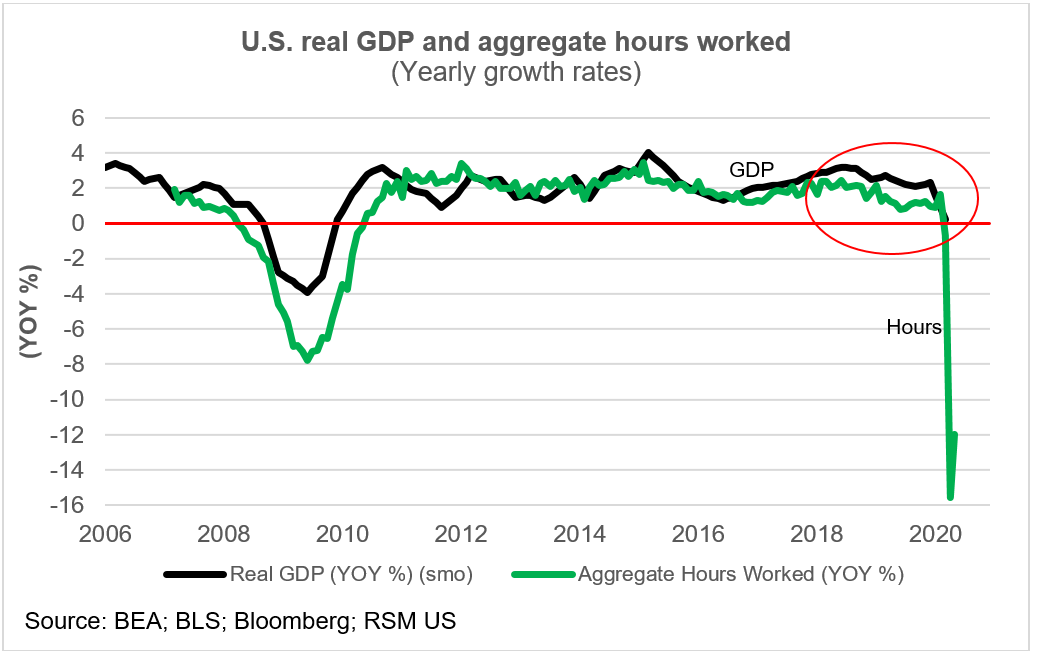

The labor sector

The labor sector has undergone a significant shock, with 45 million members of the labor force being thrown out of work in the last 13 weeks alone. The figure below shows the result of shutting down all non-essential industry and services – a dramatic, overnight drop in hours worked that will have a short- and medium-term negative effect on consumer spending habits.

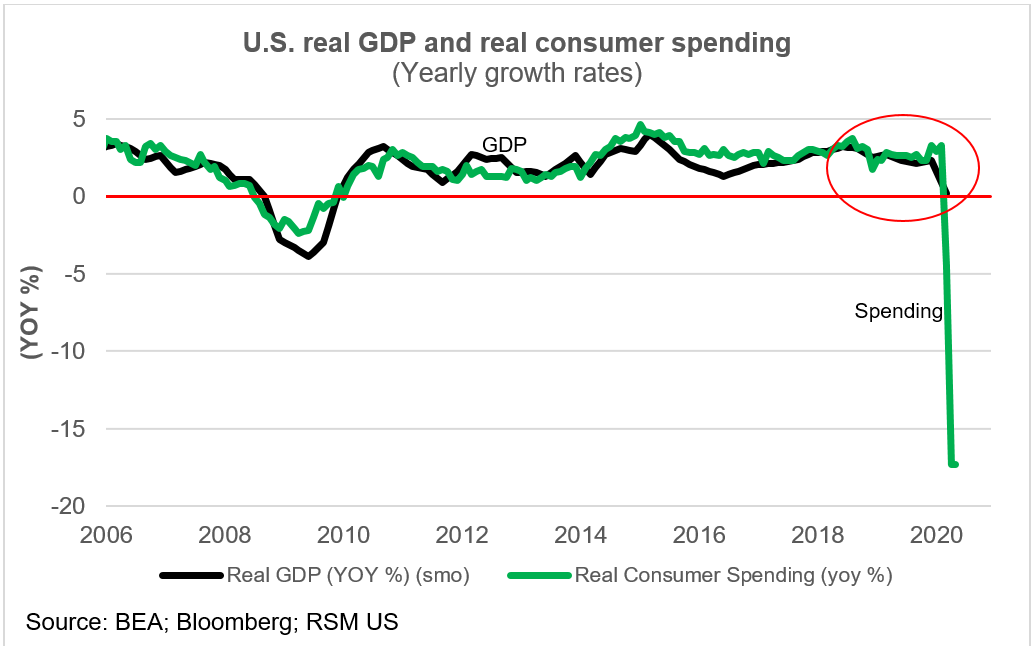

The consumer sector

With so many workers out of a paycheck, and with layoffs creeping into white-collar occupations, household spending on non-essential goods and travel and hospitality plunged during the pandemic. In inflation-adjusted terms, there was a 4% drop in real consumer spending in March, followed by a 17% decline in April.

Although states have loosened restrictions on retail shops and restaurants, the reluctance of consumers to relax social distancing practices will have an enduring impact on the way we shop and entertain ourselves.

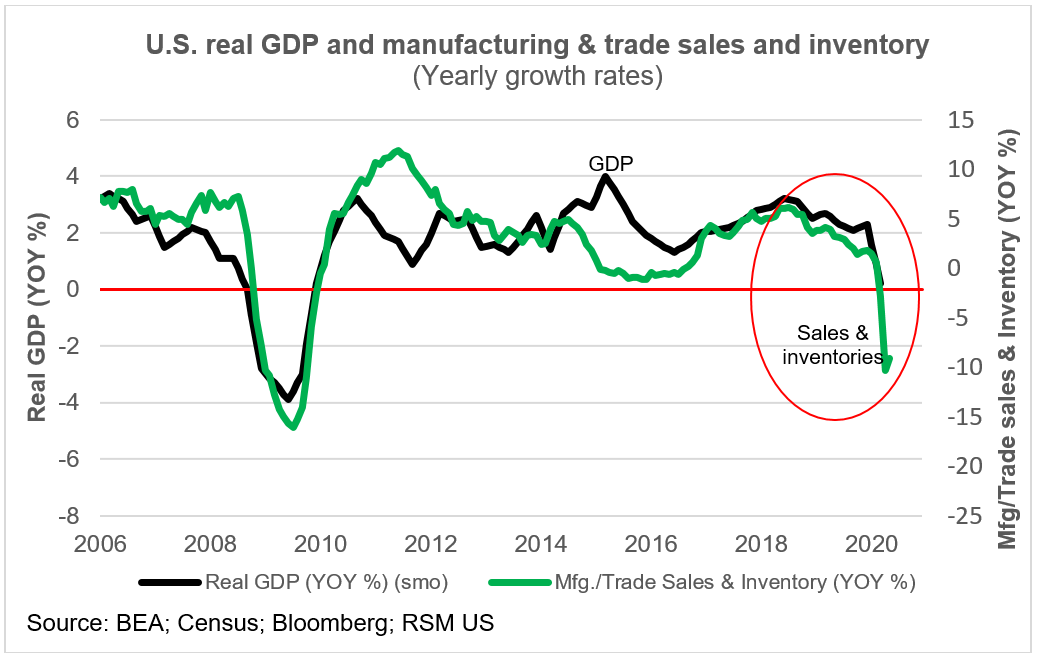

The commercial sector

As with all other sectors, manufacturing and trade sales have been in decline since the third quarter of 2018 – a testament to the end of the decade-long recovery from the Great Recession and to the assault on our rules-based system of international trade.

Inventory accumulation has been in decline for more than a year and was flat in the first quarter before losing 2% in April. Manufacturing and trade sales were also in decline, but had a slight increase in January that didn’t hold up. Manufacturing and trade sales lost nearly 5% in March followed by an 18% loss in April.

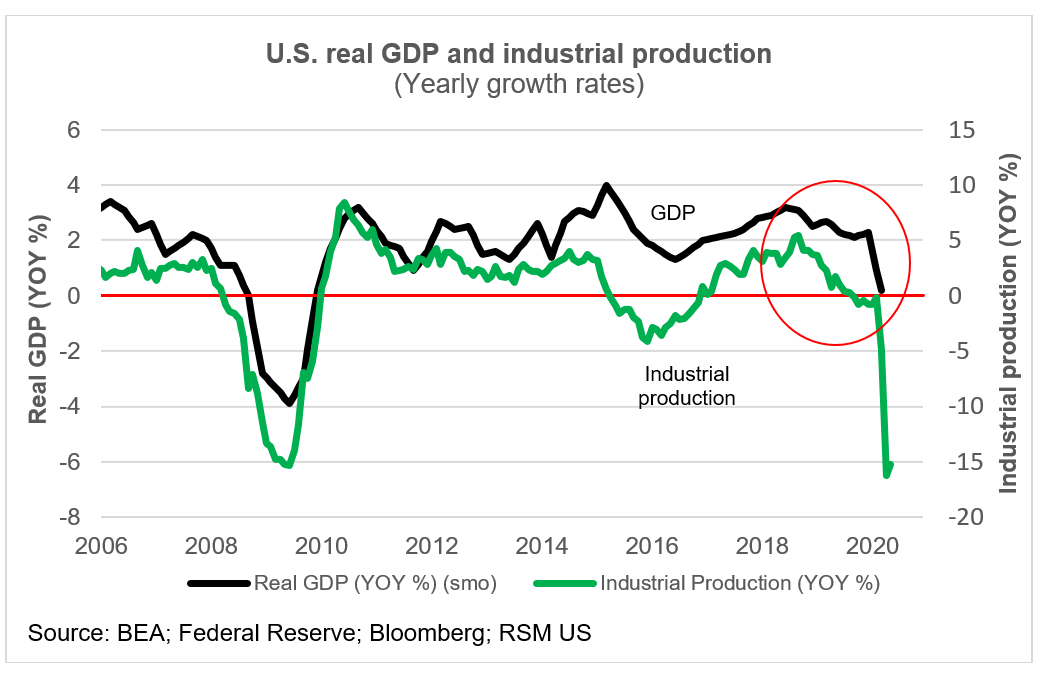

The industrial sector

As the figure below shows, the business cycle closely follows trends in industrial production. This is because of the virtuous circle of industrial growth feeding into the labor market and wages and, in turn, the growth of household spending.

Industrial production has been in decline since peaking in September 2018 and turning negative a year later in September 2019. Industrial production in March 2020 was down by 5% from the previous year, followed by a 15% drop in April and a 14% decline in May.

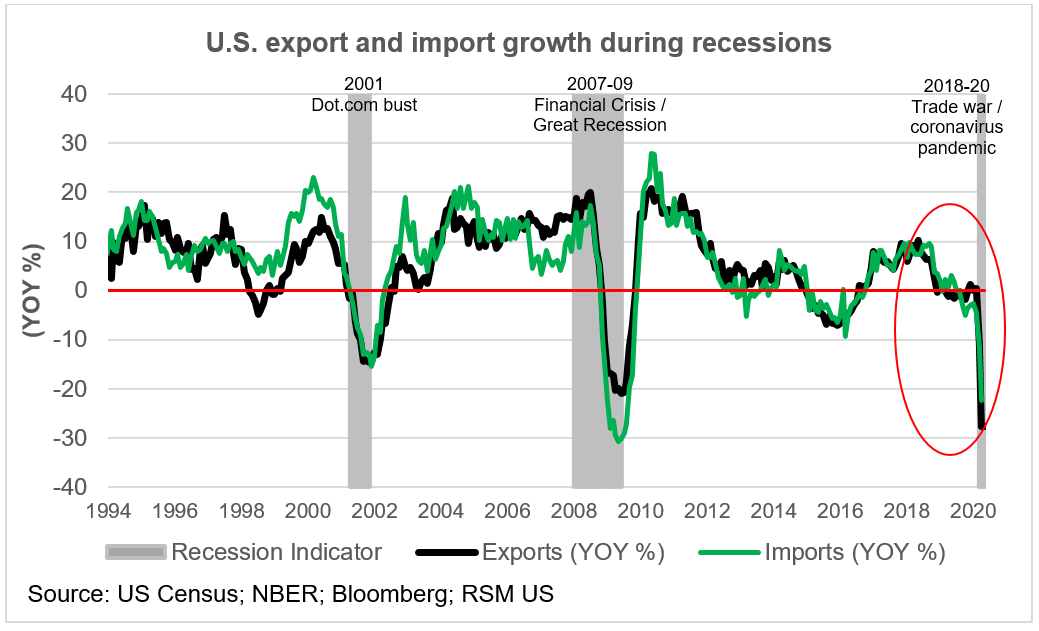

The external sector

Note that our monthly GDP index excludes the impact that the external sector can have on the national accounts. As shown in the first figure below, living in a global economy means that when demand drops (or rises) in the U.S., it is most likely the case that demand in our trading partners will follow suit. So U.S. exports and imports will tend to have similar patterns of decline during economic downturns and increases during the subsequent recovery.

From time to time, however, there will be episodes when U.S. demand for foreign goods outstrips foreign demand for our exports. Though it results in a drop in net exports and is a drag on the national accounts, this is often a positive sign that the U.S. economy is growing faster than the rest of the world and will perhaps lead the global economy out of a recession.

With our trading partners suffering the same consequences of the trade war and the pandemic, there are too many uncertainties to confidently predict divergence in those trends. For instance, how will the spread of the virus to South America and Africa affect international commerce? Will the emergence of a possible second wave of the virus in China carry over to the rest of the world?

For more information on how the coronavirus is affecting midsize businesses, please visit the RSM Coronavirus Resource Center.

Chamber members are doing great things!

Members' efforts are highlighted on our news page, and our community events feature webinars and other resources available to our business community.

Have a great story to share? Let us know! Email our Customer Success team at customers@austinchamber.com

Related Categories: COVID-19 resources, For the community, Membership